Stochastic Models

Maximum expected NPV for period 2

Minimum NPV expected for Period 2

P90 NPV for Period 3. 90% of possible expected values for Period 3 are below this point.

P10 NPV for Period 3. 10% of possible expected values for Period 3 are below this point.

Expected NPV for Period 6.

Maximum expected Cumulative NPV for Period 2.

Minimum Cumulative NPV expected for Period 3

P90 Cumulative NPV for Period 4. 90% of possible expected values for Period 3 are below this point.

Expected Cumulative NPV for Period 5.

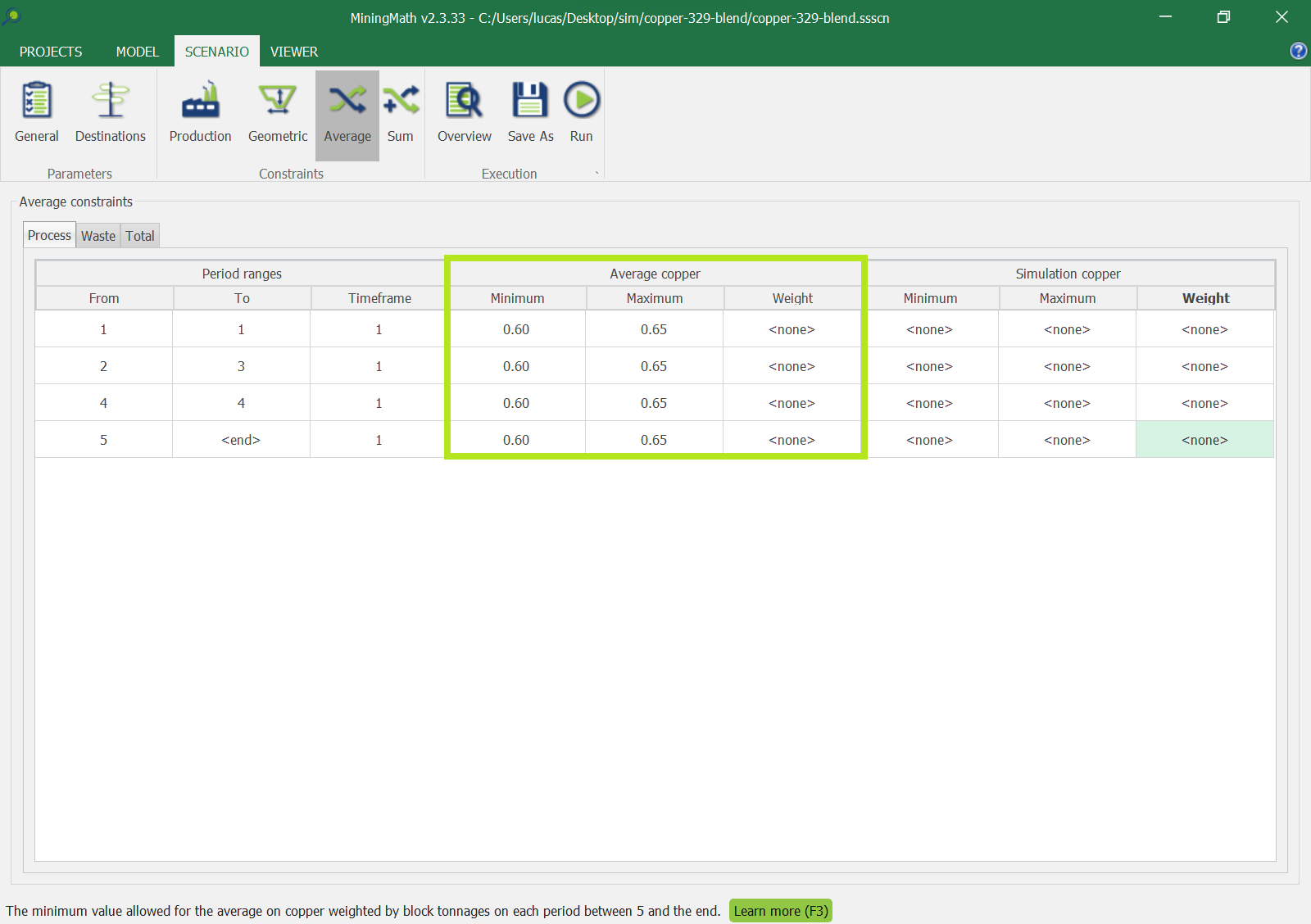

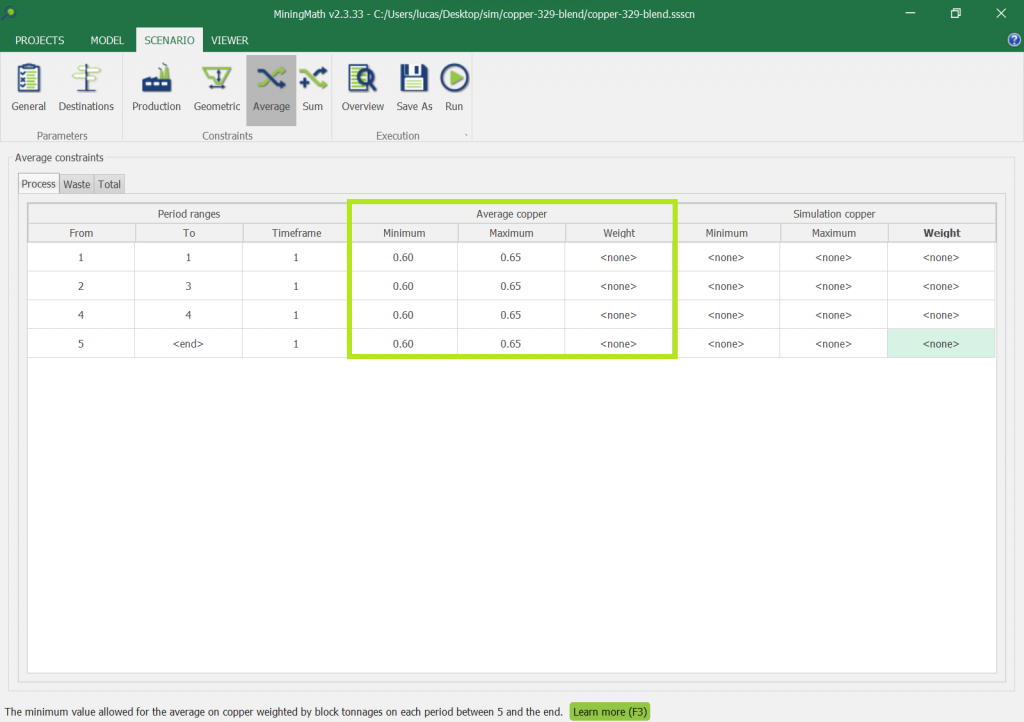

Expected values to control the averages over all simulations.

These constraints will guarantee that, in average, the indicators will be within the defined ranges. For example, take Expected Min = 0.60 and Expected Max = 0.65 for a certain constraint. If there are 3 simulations returning 0.59, 0.62 and 0.65, the average is 0.62, so this is within the range defined.

Example to control the average of all simulations. This option is only available when databases containing stochastic data are imported. All simulations to guarantee that each one of them respect certain criteria

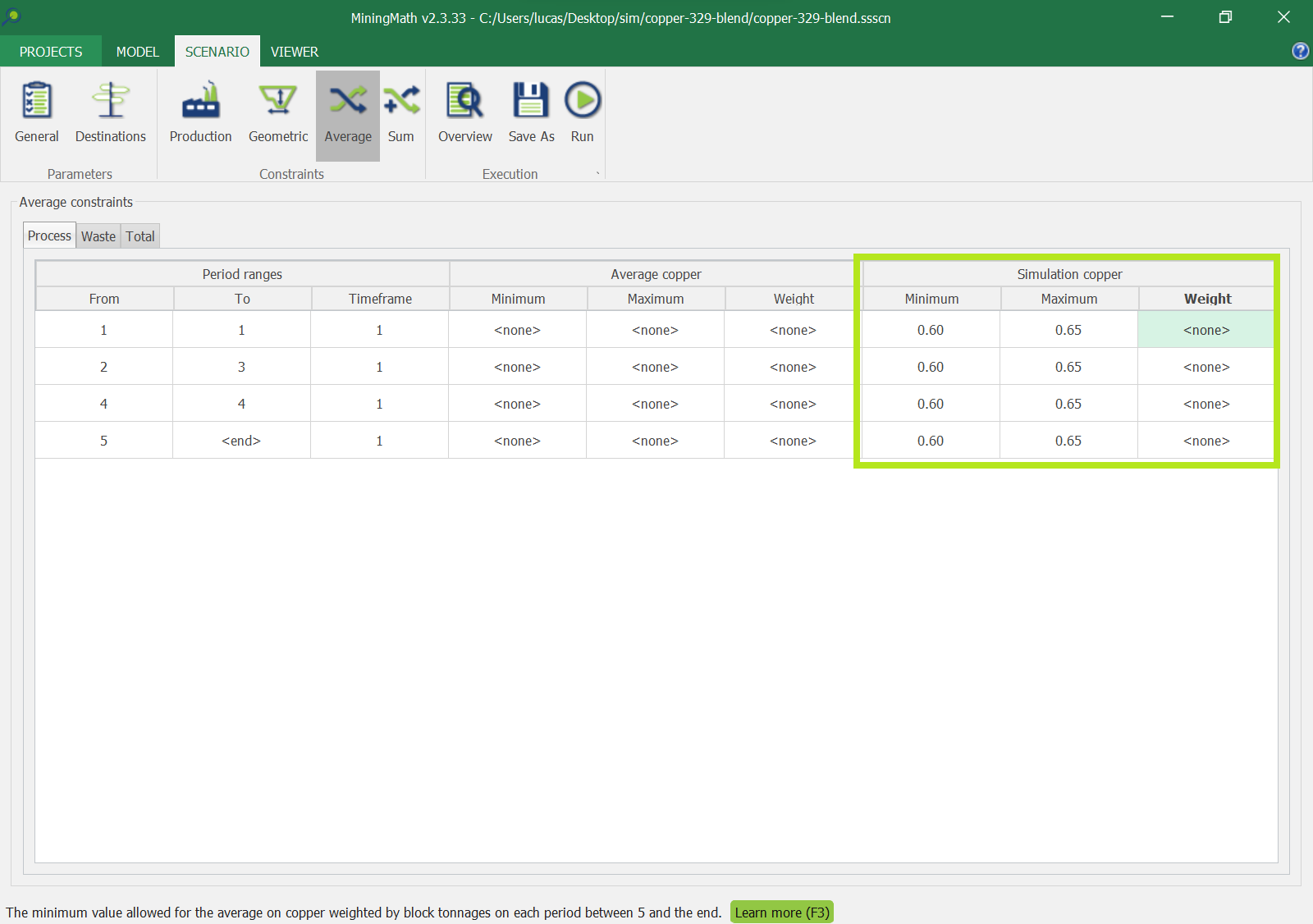

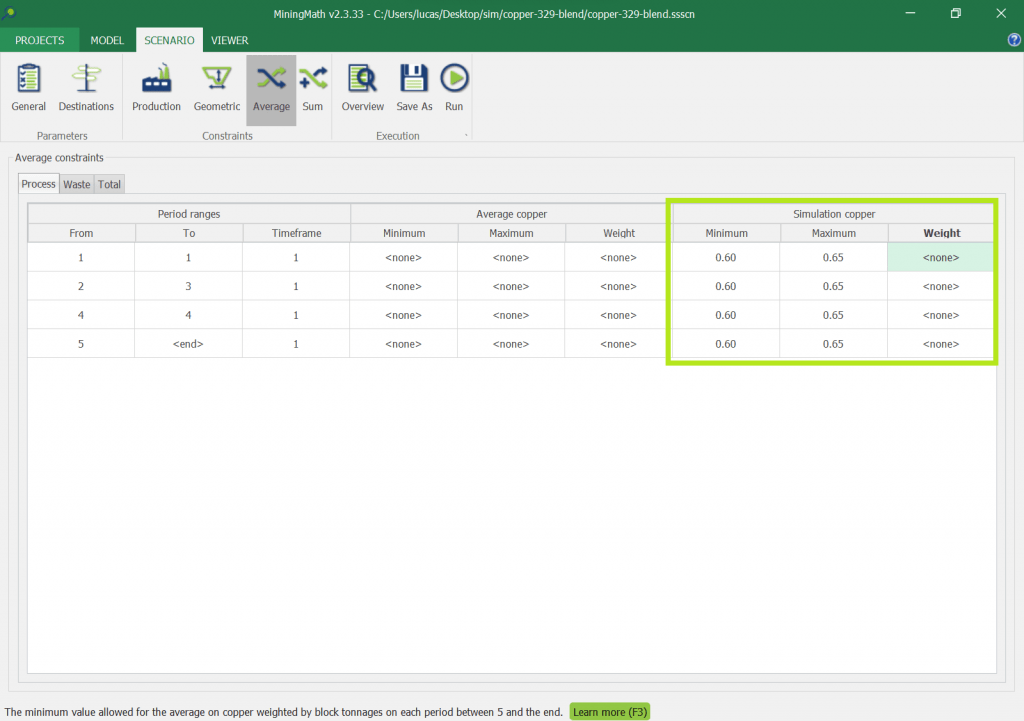

These constraints control the variability, or the spread, of the results to be within a certain acceptable range. Let's take an example where such a range has Min = 0.60 and Max = 0.65, and again three simulations returning 0.59, 0.62, and 0.65. In this case the solution will be penalized by the optimizer, as 0.59 < 0.60. Learn more about penalized solutions here.

Example to control all simulations individually. This option is only available when databases containing stochastic data are imported.